- support@locusassignments.com

Unit 9 Management Accounting Sample Assignment

Introduction

This assignment explores the classification of different types of costs in business, focusing on materials, wages, expenses, and overheads. It examines how these classifications are applied in the case of Launch Break Ltd, a bakery company. For those seeking guidance, Locus Assignments offers expert assignment help services to enhance understanding and application of management accounting concepts.

Task 1

LO1. Be able to analyse cost information within the business for the task specified

1.1 - Classify the different types of costs. How are the costs classified in the case study?

a) Classification of Cost: Classification of Cost can be made in a number of ways. For different classifications, manufacturing & service-providing units use different costing techniques.

The different costing classifications can be summarised as under:

Materials: Materials can be broadly classified as:

• Direct Material & Indirect Material

Wages: Wages can be classified as:

• Direct Wages & Indirect Wages

Expenses:

• Direct Expenses & Indirect Expenses

• Direct Material, Direct Wages & Direct Expenses together comprise Prime Cost, and Indirect Material, Indirect Wages & Indirect Expenses together are called overhead.

• Direct Materials are the materials which are directly related to production.

• Direct Wages are the cost of labour which is directly related to production.

• Direct expenses are the cost which directly varies with the production units, such as lighting & heating, fuel & power, etc.

• Overhead Expense can be broadly classified as Function-wise & Behaviour-wise.

Function-wise Classification:

• Factory/Works/Manufacturing Overhead - It includes all the indirect expenses incurred inside the factory building, such as repairing parts for the manufacturing equipment, depreciation of manufacturing equipment, electricity, rent & rates, etc.

• Administrative/General/Office Overhead - It is related to the expenses which are incurred in relation to general administration. It includes the salary of office staff, electricity for the administrative building, office equipment, office stationery, etc. (Innes and Mitchell, 1993)

• Selling Overhead - Selling overhead is the expenses which are incurred in relation to sales. It comprises the salary & commission of sales staff, advertisements, promotions, etc.

• Distribution Overhead - The expenses incurred in connection with the delivery of the product, such as delivery van expenses, salary of the delivery boy, etc.

Behaviour-wise Classification:

• Variable Overhead refers to the expenses which proportionately vary with production units, such as indirect material, indirect labour, and indirect expenses which cannot be directly allocated to a specific product.

• Fixed Overheads are the expenses which remain fixed irrespective of the production volumes and consist of rent and rates, depreciation on factory equipment, insurance, office expenses, etc.

• The expenses which partly remain fixed and partly variable with the production output are called Semi-variable or Semi-fixed Overhead.

The following formula can be used for calculating Semi-variable overhead:

Y = a + bX

Where:

Y = total mixed cost

a = total fixed cost

b = variable costs per unit

x = levels of the activities

Some examples of semi-variable overheads are telephone expenses, salary inclusive of bonuses, etc.

Marginal Costing distinguishes between the fixed and variable costs of a product. The cost of producing one additional unit is termed marginal costing. In producing one additional unit, there is no change in the fixed cost. It is to be noted that fixed and variable costs are short-term concepts. In the long run, all costs are variable.

Classification of cost can also be made in relation to the accounting period. The benefit which is derived in future periods is termed Capital Cost. Such costs have to be amortised over a number of years. On the other hand, the costs incurred solely for a particular year are called Revenue Costs. It forms part of the Total Cost incurred solely for that particular year.

Classification of Cost can also be made according to the decision-making process, such as opportunity cost, sunk cost, controllable & uncontrollable cost, joint cost, differential cost, etc.

Standard Cost: Standard costs are associated with the manufacturing companies' cost of direct material, direct labour & direct expenses. Variance analysis is an important part of standard costing which shows the actual differences between the actual cost and the standard cost. Some of the major variances are volume variation, material cost variation, labour cost variation, etc.

Value of Classification: The following are the values of classification which are given:

• Cost control and Cost reduction: Cost control and cost reduction are very important tools for an organisation to work efficiently and effectively. Cost reduction aims at reducing the unit cost of goods manufactured or services rendered. On the other hand, cost control aims at achieving pre-determined cost targets.

• Pricing of output: Sometimes the firm has to sell its products at marginal cost in order to stay in the market. Cost classification helps in making such a decision.

• Absorption of overhead: Recovery of overhead is another name for Absorption of overhead. It is the process of sharing the overhead cost of all the products of a particular department. It is the allocation of overhead to each unit of output.

• Make or buy decisions: In order to cut down costs, at times the quality management of organisations has to decide whether to make or buy any particular component in the manufacturing of a product. Due to the large availability of production capacity, such decisions have to be made. Classification of cost helps in making such decisions.

• Product diversification/expansion/discontinuation of a product line: Depending upon the profitability of the firm, the management has to decide whether to diversify their product line or not. After a particular span of time, the management of the firm should take the initiative for expansion in order to respond to rival firms’ actions.

Suitable Classification of Costs for Launch Break Ltd.:

Launch Break Ltd is a bakery company. The suitable costing method for this organisation is process costing. As most of the cost expenses are managed by various departments, it is accounted for as direct cost for the organisation except for a few items of expenses which have to be apportioned. In this process of accounting, the organisation follows the various types of production costs obtained by the department to measure the cost of production per unit. So, this process of accounting is far better than job costing.

The different types of processes used department-wise:

• Material - The first stage of the production is to issue the raw material. After the first stage of raw material is selected, other subordinate materials are mixed to follow the further process of production.

• Labour - The costs of wages of the labourers are added to the cost of that particular product or process. Common wages are to be classified and apportioned as suitable to the situation. With the help of various factors, the cost of common wages can be apportioned, e.g., wages can be apportioned according to the time spent on the production of a product per unit

• Direct expenses - Direct expenses are those which are completely attributed to the production of a specific product. These expenses are directly debited to the process. Some exceptions to direct expenses are hire charges, electricity, depreciation, etc.

• Overhead expenses - These expenses are not directly included in the production but are absorbed on the basis of an absorption rate. In other words, these are the indirect costs to a company or organisation. Heads of such expenses may include rent, maintaining plant and machinery, etc.

Need help with your assignments? Get top-notch assistance from Locus Assignments' expert team offering UK assignment help services tailored to your needs!

1.2 - What are the different costing methods? Identify and explain the costing method used by Launch Break Ltd.

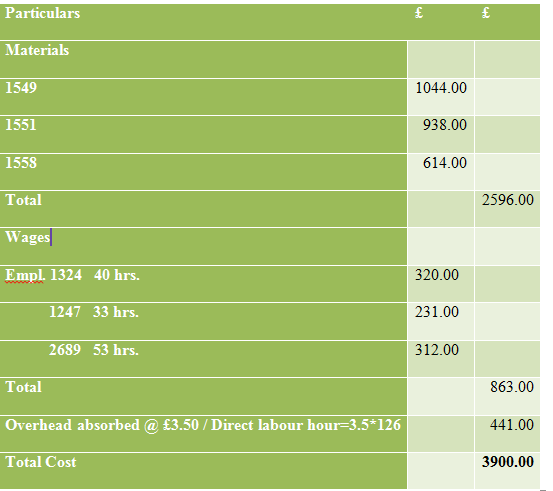

a) Calculation of Cost of Job no. 336

b) Costing Methods

There are various methods for computing the cost of production, cost of sales, unit cost, etc. The organisation or the company has the right to choose what kind of methods they are going to adopt for their production depending upon the output. These types of methods can be classified as listed below

(i) Single or Output Costing: This method is adopted to ascertain the cost of a single unit of production. This method is also applied when there is the production of the same identical units. To determine or to obtain the cost per unit, cost statements or cost sheets are prepared. In this method, the various expenses are classified, and the total expenditure is divided by the total quantity produced to determine the cost per unit. This method is generally suitable for brick-making collieries, flour mills, paper mills, cement manufacturers, etc

(ii) Contract Costing: Contract costing is the specific form of order costing. Generally, an organisation gives a contract when and where work is undertaken by a customer with some special requirements and for a longer period of time. These works are generally done outside. Such contracts are termed contract costing. Examples of such contract costing can be building construction, shipbuilding, civil construction, etc. (Madegodwa, 2007)

(iii) Job Costing: Job costing refers to those methods of costing where the basic method of costing is applied. These are mainly applicable to those industries or firms where the work contains different contracts and jobs. This follows an order-specific costing technology, which helps in using different situations of different jobs with specified customer specifications. Job costing helps in keeping both indirect and direct costing accounts. Job costing methods are similar to contract costing and batch costing.

(iv) Process Costing: Process costing is the accumulated cost prepared in a stage of process or production. Here, the cost per unit of a certain product is ascertained at every stage of production by dividing the cost of each process by the normal output unit of the process. CIMA London explains process costing as “that form of operation costing which applies where standardised goods are produced”. These methods can be used in industries like chemicals, petroleum, textiles, rubber, sugar, coal, etc.

(v) Operating Costing: Operating costing refers to those costs where expenses are associated with the administrative business. In simple words, these expenses are incurred by the firm or an organisation on a daily or day-to-day basis. These costs are a mixture of both fixed costs and variable costs. Fixed costs are those costs which remain the same even if the number of production exceeds the actual production, whereas variable costs can vary irrespective of the quantity produced.

(vi) Multiple Costing: In a multiple costing system, the cost of different sections of production is mixed after finding out the cost of each and every part of the produced goods. With the help of an assembled computer, one can ascertain the variable cost of multiple costs, as different parts of the computer have different manufacturing costs. The various components differ in variety in terms of price, material, and manufacturing process. The manufacturing entity uses a separate method for costing employment in respect of each part.

1.3 - How is the cost calculated, using appropriate techniques? What is the costing technique used by the organisation to calculate its costs?

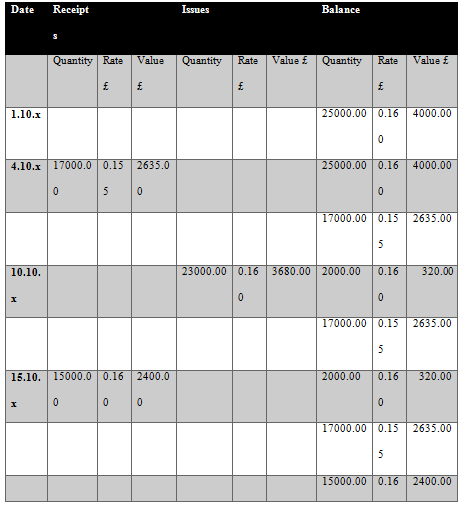

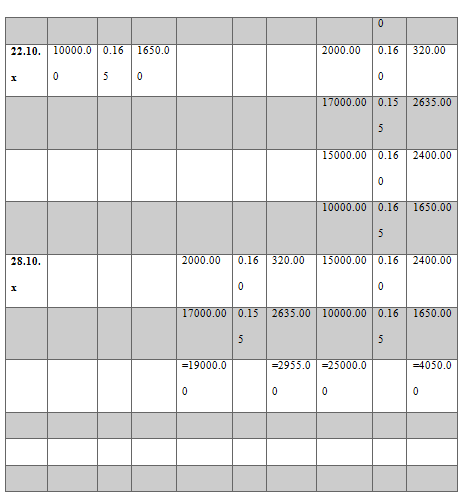

a) First In First Out

Stores Ledger Account (FIFO)

Closing Stock 25000 units=£4050

b) Direct Labour Cost

Direct Labour Cost:

Standard hours for production are 11250 hrs.

Actual hours worked 10750 hrs.

Hours saved 11250-10750 500 hrs.

Cost of Direct Labour

Normal wages = 10750*8 £86000

Bonus = .75*8*500 3000

50% of over-time premium

=50% of 2*2400 2400

Total £91400

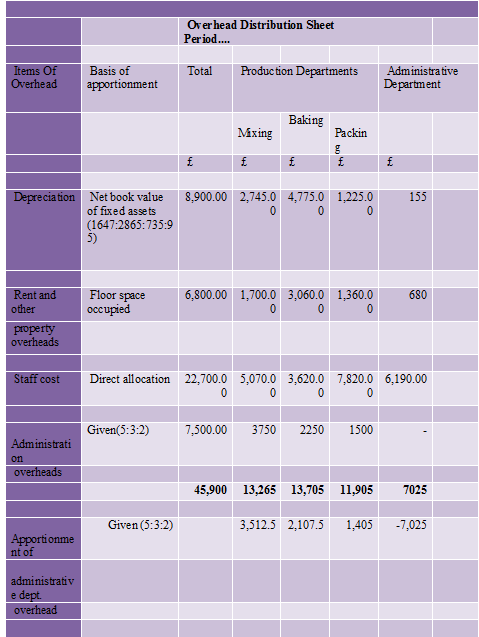

c) Overhead Analysis

d) (i) Budgeted Fixed Overhead Absorption Rate

d) (ii) Distinction between Costing Method and Costing Techniques:

Methods indicate an integrated system applied depending upon the manufacturing technique. The term refers to the cost ascertainment of different methods of costing by different industries. The following are some important methods of costing:

• Job Costing

• Process Costing

Job Costing - Another name for job costing is terminal costing or specific order costing. Costs are accumulated according to the job or work order. The material, labour and overhead costs are allocated through respective abstracts which are charged on a predetermined basis. Job Costing can be further classified as under:

• Contract Costing

• Cost-plus Contract

• Batch Costing

Contract Costing - This method of costing is applicable where the job work is big, like a contract for a bridge. Under this method, costs are collected according to each work order.

Cost-plus Contract - The contracts which provide for the payments of the actual cost of contracts plus a marginal profit. These profits are to be added to the cost. Such profits may be fixed or a stipulated percentage over cost. These contracts are generally entered into when the actual cost of contracts cannot be determined with reasonable accuracy due to low availability of materials, labour etc., or elsewhere the contract is extended for a long period of time.

Batch Costing - Batch Costing is applicable where the production is carried out in batches. For each batch, a separate cost sheet is maintained assigning separate batch numbers. Batch Costing is mainly carried out in drug industries, ready-made garments industries, etc.

Process Costing - The continuous operation of a product through different processes is termed process costing. This costing method is applicable when the product passes through different processes and is converted into a finished product. The process costing method is mainly applicable in the cement industry, sugar industry, textile industry, etc. Process costing can be broadly classified into:

• Operation Costing

• Operating Costing

• Output Costing

• Multiple Costing

Costing Techniques - Cost control, cost ascertainment and allocation of expenditure are powerfully achieved through the help of costing techniques. It is helpful in the supply of information to the management. The following are the various techniques of costing:

• Uniform Costing

• Marginal Costing

• Standard Costing

• Historical Costing

• Absorption Costing

Uniform Costing - When the same costing concepts/principles are used by several undertakings, they are said to be following uniform costing. The adoption of a common method of costing by different organisations is the main objective of uniform costing.

Marginal Costing - The costing technique which aims at ascertaining the marginal cost by determining the changes in cost, volume, price, etc., is termed marginal costing. It is achieved by segregating total costs into variable and fixed costs.

Standard Costing - Standard costs are associated with the manufacturing companies' cost of direct material, direct labour & direct expenses. Variance analysis is an important part of standard costing which shows the actual differences between the actual cost and the standard cost. Some of the major variances are volume variation, material cost variation, labour cost variation, etc. (Madegodwa, 2007)

Historical Costing - Recording of actual costs after they have been incurred is termed historical costing. Material cost, labour cost, and overhead cost together comprise the actual cost.

Absorption Costing - It is the technique of charging all variable and fixed costs to operations, products, processes or services. Absorption Costing is also termed as Full Costing.

d) (iii) In the case of Launchbreak Ltd, any one of the techniques discussed above can be adopted, as only marginal costing and absorption costing differ in the treatment of fixed production overheads in the accounting records and managing financial statements.

1.4 - Analyse the cost data of the organisation focusing on the technique used for the purpose

Statement of Cost for October:

In the above statement, the material cost incurred for preparing 45,000 units of cake is £17,200, which includes £6,880 for flour and £10,320 for other materials. The hours worked by labourers in the different production departments are: Mixing - 3,800, Baking - 2,050, Packing - 4,900, and the normal rate for working an hour is £8. Therefore, the labour cost incurred for producing 45,000 units of cake is £86,000, i.e. 3,800+2,050+4,900=10,500×£8=£86,0003,800 + 2,050 + 4,900 = 10,500 \times £8 = £86,0003,800+2,050+4,900=10,500×£8=£86,000.

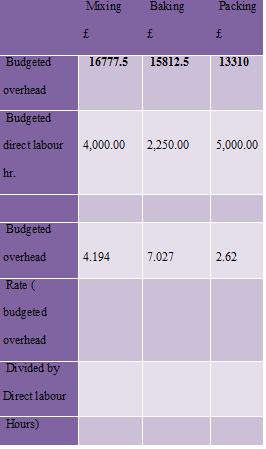

Overhead absorption in the product is an important aspect which an account manager needs to know. The overhead absorption rate is derived for each department by dividing the total overhead amount of each department by their labour hours. Hence, the overhead absorption rate for each department is:

• Mixing department - £4.194/hour

• Baking department - £7.027/hour

• Packing department - £2.62/hour

Therefore, the overhead cost absorbed by each department for producing 45,000 units of cake is:

• Mixing department - £15,937.2

• Baking department - £14,405.35

• Packing department - £12,838

The total cost incurred for producing 45,000 units of cake is £146,380.55, and the cost per cake is derived by dividing the total cost incurred for producing 45,000 units of cake by 45,000 units of cake produced, i.e. £146,380.55 / 45,000 units of cake = £3.2529 per cake.

Need help with your accounting assignment? Upload assignment details to Locus Assignments, we have a dedicated team of academic writers with years of experience in this field. Our expert assignment helpers will assist you with all your accounting assignments.

Task 2

LO2. Be able to propose methods to reduce costs and enhance value within the business

2.1 - How are the cost reports prepared and analysed for Launch Break Ltd

a) Challenges in preparing Routine Cost Reports: The Cost of Production Report (CPR) shows all costs chargeable to a department. At the end of each month, journal entries are not only the source for a summary at the end of each month or a period but also an effective means of presenting and disposing of accumulated costs during the period. Managerial purposes will not be solved by only identifying the total cost. The costs are to be divided in detail to facilitate cost control and cost reduction.

b) Cost Report Strategy of Launch Break Ltd.: Lunch Break Ltd has adopted the Standard Costing technique along with the absorption costing system. Since direct labour is a significant input, overheads are being absorbed based on direct labour hours.

2.1 - What are the various performance indicators used by the organisation to identify its potential improvements

a) Target Ratios of Takeaway

b) (ii) Limitations of Use of Ratios: There are some limitations of financial ratios that an analyst should take care of:

• Many large companies operate differently in different divisions of industries. For such companies, it is difficult to find a meaningful set of industry-average ratios.

• Different accounting practices can disturb the comparisons even within the same company (leasing versus buying equipment, LIFO versus FIFO, etc.).

• It is difficult to find out whether a ratio is good or not. A high cash ratio in a historically assessed growth company may be interpreted as a good sign, but it may also be seen as a sign that the company is no longer a growth company and should command lower valuations.

2.2 - To the chosen case study, identify and discuss the different cost reduction and value enhancement strategies available and how they can be implemented within Launch Break Ltd.

Launch Break Ltd can go away with the decision to purchase Takeaway Ltd. As the ratios of Takeaway Ltd are quite satisfactory, even if the profit percentage is not up to the mark, it has the scope for cost reduction. In order to earn a greater profit, initiatives should be taken to reduce the cost. There are some ways of achieving it, by increasing the sales per customer and efficiently utilising the money spent. Increasing larger returns from sales promotions and advertising. (Hansen and Palmer, 1997)

Sometimes, in order to earn a greater profit, it is difficult to cut down the expenses. If the sales are increased substantially, the cost per percentage of sales substantially declines.

The Profit and Loss statement provides a summary of expenses and helps in locating expenses that can be cut. Therefore, the information should be as current as possible. For this reason, a monthly Profit and Loss Account needs to be prepared.

Task 3

LO3. Be able to prepare forecasts and budgets for a business

3.1 - Explain the purpose and nature of the budgeting process adopted

Purpose and Nature of Budgeting Process: The budget process starts with the formulation of a budget. It finds out the resources needed to operate its programme during a particular year. Budgeting is the process of financial planning and control by using estimated financial and accounting data. The ICWA of the UK defines a budget as “a financial and/or quantitative statement, prepared and approved prior to a defined period of time, of the policy to be pursued during the period for the purpose of attaining given objectives.” It may include income, expenditure, and the employment of capital.

Key factor: While making a budget, there are some factors which set out the limitations in making the quantity produced for sale. This is known as the Key Factor or Limiting Factor. The ICWA (UK) defines a factor as “the factor the extent of whose influence must first be assessed in order to ensure that the functional budgets are reasonably capable of fulfilment.” From the viewpoint of sales, there are many factors by which demand is influenced, such as price, quality of the product, and purchasing power of the customers. The key factor in production may be plant capacity, availability of labour, and availability of raw material.

3.2 - What is the budgeting method used and reflect its needs

a) Methods of Budgeting:

• Fixed Budget: As defined by the ICWA London, a fixed budget is a budget which is designed to remain unchanged irrespective of the level of activity actually attained. It is employed when budgeted output is close to the actual output. Maximum managerial control can be exercised by making comparisons with actual operating results. (Vatter, 1969)

• Flexible Budget: ICWA, UK defines a flexible budget as “a budget which by recognising the difference between fixed, variable, and semi-fixed costs, is designed to change in relation to the level of activity attained.” A flexible budget is prepared for more than one level of activity.

b) Zero-base Budgeting: Zero-base budgeting is the process of traditional budgeting which makes planning and decision-making easier for an organisation. The term Zero-base budgeting is the practice of budgeting for every unit of income received. Zero-base budgeting also includes the identification of tasks and funding resources for the completion of the task.

Advantages of Zero-base Budgeting:

• It helps in the allocation of resources more efficiently and smoothly and helps in finding out new ways by which costs can be reduced effectively.

• It gives motivation, communication, and coordination by which wasteful operations can be identified and rectified or controlled.

• It also helps in finding out alternative courses of action.

Disadvantages of Zero-base Budgeting:

• As it is the conventional way of budgeting, it consumes more time for its implementation.

• Justification of every item is not possible by the use of zero-base budgeting.

• It also requires qualified persons for its implementation. (Vatter, 1969)

c) Rolling Budget: A rolling budget, also known as a continuous budget or perpetual budget, is one in which the budget period automatically extends continuously, incorporating the changes in the budget. It adds future accounting periods to replace budgets for an accounting period that has passed.

Advantages:

• It helps to be responsive to unexpected changes.

• It is more up-to-date than a conventional static budget.

Disadvantages:

• Constant revisions may cause distraction and disturbances for the employees.

• The main disadvantage of rolling a budget is that it is akin to preparing a new budget again and again. (Doerr, 1991)

d) What-If Analysis: The other name of What-If Analysis is Sensitivity Analysis, which helps in planning, decision-making, and managing a business. The management knows the use of what-if analysed beforehand and what changes are going to take place in the future, and on the basis of that, the budget is prepared.

3.3 - As an accounts manager, prepare the required budgets

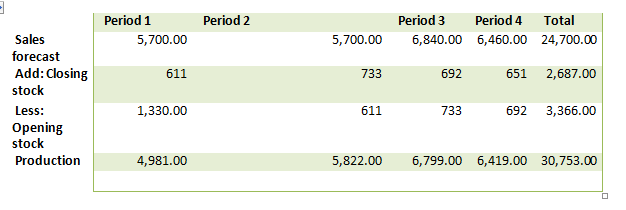

a) Production Budget

b) Material Purchase Budget

|

|

|

|

|

|

|

|

|

Period 1 |

Period 2 |

Period 3 |

Period 4 |

Total |

|

Standard consumption |

6 gm/unit |

6 gm/unit |

6 gm/unit |

6gm/unit |

|

|

Production |

491units |

5822 units |

6799 units |

6419 units |

24021 units |

|

Purchase |

29886 gms. |

34932 gms. |

40794 gms. |

38514 gms |

144126 gms. |

|

|

|

|

|

|

|

c) Cost of Material

|

|

Period 1 |

Period 2 |

Period 3 |

Period 4 |

Total |

|

Value £ |

239088.00 |

279456.00 |

326352.00 |

308112.00 |

1153008.00 |

d) Labour Hour Budget

|

|

Period 1 |

Period 2 |

Period 3 |

Period 3 |

Total |

|

Labour hour required @ 2 hrs. Per unit Labour hour available |

9962 12480 |

11644 12480 |

13598 12480 |

12838 12480 |

48042 4920 |

e) Labour Cost Budget

|

|

Period 1 |

Period 2 |

Period3 |

Period4 |

Total |

|

Normal wages£ |

39848 |

46576 |

49920 |

49920 |

186264 |

|

Overtime |

|

|

6708 |

2148 |

8856 |

|

Total |

39848 |

46576 |

56628 |

52068 |

195120 |

3.4 – Illustrate the cash flow forecast for Launch break and comment on its findings

|

|

Sept.13 £ |

Oct. 13 £ |

Nov. 13 £ |

Dec. 13 £ |

Jan. 14 £ |

Feb. 14 £ |

|

Cash balance |

5000.00 |

8440.00 |

29840.00 |

-16560 |

-5440 |

7720 |

|

Add: Cash sales 40% less 10% discount |

18240.00 |

15200.00 |

17100.00 |

16720.00 |

15960.00 |

19000.00 |

|

Collection from debtors |

30000.00 |

28800.00 |

24000.00 |

27000.00 |

26400.00 |

25200.00 |

|

Sale of assets |

---- |

8000.00 |

---- |

---- |

----- |

---- |

|

Total |

53240.00 |

60440.00 |

70940.00 |

27160.00 |

36920.00 |

51920.00 |

|

Less: Purchase |

16000.00 |

17600.00 |

20000.00 |

19200.00 |

16000.00 |

18000.00 |

|

Wages fixed |

2000.00 |

2000.00 |

2000.00 |

2000.00 |

2000.00 |

2000.00 |

|

variable |

4800.00 |

4000.00 |

4500.00 |

4400.00 |

4200.00 |

5000.00 |

|

Fixed cost |

7000.00 |

7000.00 |

7000.00 |

7000.00 |

7000.00 |

7000.00 |

|

Corporation tax |

----- |

----- |

44000.00 |

---- |

---- |

---- |

|

Purchase of assets |

15000.00 |

----- |

10000.00 |

---- |

---- |

4000.00 |

|

Total |

44800.00 |

30600.00 |

87500.00 |

32600.00 |

29200.00 |

36000.00 |

|

Cash balance |

8440.00 |

29840.00 |

-16560.00 |

-5440.00 |

7720.00 |

15920.00 |

Struggling with your coursework? Get assistance from expert assignment helpers at Locus Assignments and achieve academic success with UK assignment help services.

Task 4

LO4. Be able to monitor performance against budgets within the business

4.1 How are the variances calculated? Identify possible causes and recommend corrective action

a) Calculation of Various Information

(i) Actual price of material per gram = 143000.00/27500 = £5.20 per gram

(ii) Standard usage of material for actual production:

Standard quantity per unit = 30 gms.

Thus, standard usage for actual production

= 30 gms * 900 = 27000 gms.

(iii) Actual labour rate per hour

= 26040.00/4200 = £6.20 per hour.

(iv) Standard labour hour for actual production = Standard labour hour per unit * actual units produced.

= 5 * 900 = 4500 hrs.

(v) Budgeted production overhead = Budgeted output * budgeted overhead per unit of output

= 1000 * 20 = £20000.00

b) Variance Calculation

(i) Material price variance

= (Standard price - Actual price) * Actual quantity

= (5 - 5.2) * 27500 = £5500 (A)

(ii) Material usage variance

= (Standard quantity - Actual quantity) * Standard price

= (27000 - 27500) * 5 = £2500 (A)

(iii) Labour Rate variance

= (Standard rate - Actual rate) * Actual hours

= (6 - 6.2) * 4200 = £840 (A)

(iv) Labour efficiency variance

= (Standard hours for actual output - Actual hours) * Standard rate per hour

= (5 * 900 - 4200) * 6 = (4500 - 4200) * 6 = £1800 (F)

(v) Fixed overhead expenditure variance

= Budgeted fixed overhead - Actual fixed overhead

= 20000 - 23000 = £3000 (A)

(vi) Fixed overhead volume variance

= Recovered overhead - Budgeted overhead

Recovered overhead:

Budgeted overhead = £20000, Budgeted labour hour = 4500 hrs.

Thus, overhead recovery rate per labour hour = 20000 / 4500 = £4.44 per labour hr.

Actual hours worked = 4200 hrs.

Thus, overhead recovered = 4.44 * 4200 = £18667

Thus, volume variance = 18667 - 20000 = £1333 (A)

(vii) Fixed overhead capacity variance

= Standard overhead - Budgeted overhead

Standard overhead = Standard rate per unit * Standard output for actual time

= (20000 / 1000) * (1000 / 4500) * 4200 = £18660

Thus, capacity variance = 18660 - 20000 = £1340 (A)

(viii) Fixed overhead efficiency variance

= Recovered overhead - Standard overhead

= 18667 - 18660 = £7 (F)

c) Causes of Variance

MATERIAL VARIANCE:

• Material price variance: Such variances occur when raw materials are purchased at a price different from the standard price. It is that portion of direct materials cost variance which is due to the difference between the standard price specified and the actual price paid. (Fleischman and Tyson, 1998, pp. 92–119)

• Material usage variance: Material usage variance is determined as a deviation of standard quantity and the actual quantity of a given standard price per quantity.

• Material mix variance: Such variance occurs due to the difference between the standard and actual composition of the mixture.

• Material yield variance: Such variance occurs due to the difference between the standard yield specified (in terms of actual output) and the actual yield obtained. (Kaplan, 1975, pp. 311–337)

LABOUR VARIANCE:

• Labour efficiency variance: Such variances occur when labour operations are either more efficient or less efficient than standard performance.

• Labour rate variance: Such variance occurs when the actual direct labour hour rate differs from standard rates.

• Labour mix variance: Such variance occurs when a standard mix of labour (different grades) differs from the actual mix.

• Labour yield variance: Such variances occur when standard output differs from actual output.

OVERHEAD VARIANCE:

• Overhead expenditure variance: Such variances occur when the actual cost incurred differs from the budgeted cost, i.e., the cost that should have been incurred.

• Volume variance: Such variances occur due to the difference between the standard cost of overhead absorbed and the standard overhead allowed for that output.

• Capacity usage variance: This variance shows the effect of working above or below the capacity.

Management Action:

In a standard costing system, actual results are compared with the standard, and the variances, either favourable or adverse, are determined. The reasons for such variances are found, and the person(s) or department(s) responsible are identified, and responsibilities fixed.

For material cost variances, the purchasing department, production department, and stores department might be responsible. The management takes necessary remedial action. Similarly, for labour or overhead variances, responsibilities are fixed, and corrective actions like training, motivation of workers, proper sequencing of machinery, etc., are resorted to by the management. Similar remedial actions are taken for variances in overhead costs. Variances obtained under the standard costing system have to be reported to management as “management by exception” for taking remedial steps and action.

4.2 Reflect on the operating statement and how it is reconciled with the budget and actual result

|

|

|

|

|

|

|

|

|

|

|

Standard |

|

|

Actual |

|

|

|

|

|

Qty. |

Rate |

Amt. |

Qty. |

Rate |

Amt. |

Difference |

|

Direct material |

27,500.00 |

5.00 |

137,500.00 |

27,500.00 |

5.20 |

143,000.00 |

5,500.00 |

|

Direct Labour |

4,200.00 |

6.00 |

25,200.00 |

4,200.00 |

6.20 |

26,040.00 |

840.00 |

|

Overhead |

900.00 |

20.00 |

18,000.00 |

900.00 |

25.55 |

23,000.00 |

5,000.00 |

|

Total |

|

|

180,700.00 |

|

|

192,040.00 |

|

|

|

|

|

|

|

|

|

|

4.3 Comment on the report findings and address as instructed in the assessment criteria

The following points emerge after analysing the variances and operating statements.

• Material cost variance is adverse; all the variances under material cost are adverse. The purchase manager might be responsible, as it might so happen that the quality of the material is not up to the mark. Also, the purchase price of the material is higher than estimated.

• Labour rate variance has occurred in an adverse balance, but labour efficiency variance has occurred in a favourable balance. This means that although the actual labour rate is higher than budgeted, the actual productivity of labour is higher than the standard.

• All overhead variances, except overhead efficiency variance, are adverse. It is clear that management should take care to rectify the mismanagement in utilising overhead costs. (Kaplan, 1975, pp. 311-337)

Ready to get started? Upload assignment details to Locus Assignments and let our experts write it for you.

References

• Doerr, W. W. 1991. What--if analysis. Risk assessment and risk management for the chemical process industry.

• Fleischman, R. K. and Tyson, T. N. 1998. The evolution of standard costing in the UK and US: from decision making to control. Abacus, 34 (1), pp. 92--119.

• Hansen, B. G. and Palmer, A. J. 1997. FRAN, Financial Ratio Analysis and more. Radnor PA (5 Radnor Corp CTR Suite 200, Radnor 19087-4585): U.S. Dept. of Agriculture, Forest Service, Northeastern Forest Experiment Station.

• Harington, D. 1992. Costing. Open College.

• Innes, J. and Mitchell, F. 1993. Overhead cost. London: Academic Press.

• Jarett, I. M. and Brady, P. A. 1976. A Conference on key factor analysis. Carbondale: Published for the Program and the School by Southern Illinois University Press.

• Kaplan, R. S. 1975. The significance and investigation of cost variances: survey and extensions. Journal of Accounting Research, pp. 311--337.

• Madegodwa, J. 2007. Cost accounting. Mumbai: Himalaya Publishing House.

• Vatter, W. J. 1969. Operating budgets. Belmont, Calif.: Wadsworth Pub. Co.

Need Help with Your Assignment?

Get expert guidance from top professionals & submit your work with confidence.

Fast • Reliable • Expert Support

Upload NowDetails

Share this Solution

Other Assignments

Related Solution

Other Solution

We have established a strong reputation

in online education and tutoring services.

- No countries available